The looming threat of a Super El Niño this summer will add to the pressures on the agricultural industry already stressed by fertiliser shortages, inflation, and oil price hikes by adding a further systemic shock to the cost of consumers’ shopping baskets.

Up to

Under an "Extreme El Niño" scenario, global agricultural production could drop by 14.3%, resulting in an estimated $342.2 billion in lost production value (at 2025 prices).

Up to

We could see simultaneous price shocks of 10% to 50% across major food crops, with the most severely impacted commodities (like rice, palm oil, sugar cane, and coffee) potentially surging by 50% to 100%.

Up to

Just four crops—wheat, rice, maize, and soybeans—account for over 60% of all global calories, meaning a correlated weather failure across multiple continents threatens the core of the world's food supply.

El Niños are a routine part of our weather cycle – on average every seven years the trade winds weaken allowing a warmer current to flow east in the Pacific Ocean affecting the weather worldwide. Over the past century they have caused minor fluctuations in food production in multiple agricultural regions, from China to Latin America.

Once in a while, a more severe version of el Niño causes wildfires, storms and significant food production shortages in more parts of the world. The weather forecasters are worried: the signals they are picking up now suggest that the el Niño that is developing could be a particularly strong one, attracting media headlines as ‘Super’, ‘Supercharged’ and even ‘Godzilla el Niño’.

Three reasons why the possibility of an extreme El Niño must be taken seriously:

The weather patterns being predicted include hotter temperatures over key food production regions including China, India, Australia, Latin America and the Pacific Northwest and upper Midwest of North America. Forecasts include droughts and lengthy periods of below-average rainfall in swathes of southeast Asia, Central America, and potentially a failure of the monsoon rainfalls of the Indian subcontinent.

Weather anomalies are expected from July onwards, strengthening over the later summer and early fall, to be making headlines throughout the winter and new year and into the key growing seasons of spring in the northern hemisphere. The effects could persist into 2027 and 2028.

Risilience has combined forecast data for the likely El Niño weather patterns with its models of agricultural science and market dynamics. We group the likely outcomes into three scenarios:

|

|

Impact on Global Agricultural Production (Tonnes) |

Value of Lost Production (at 2025 prices) |

|---|---|---|

|

S1 Super el Niño - 1982/83 or 1997/98 |

-3.7% |

$77.5 Bn |

|

S2 Severe el Niño - 1877 |

-9.1% |

$192.9 Bn |

|

S3 Extreme el Niño with Northern Hemisphere Heatwave |

-14.3% |

$342.2 Bn |

Table 1: Impact of Scenarios on Global Agricultural Production

Global food production is a complex system. While it consists of thousands of crop types, the bulk of its value is in around 50 primary source crops. Just four - wheat, rice, maize and soybeans - account for over 60% of global calories.

When a global event like an El Niño occurs, the simultaneous impacts of weather anomalies in multiple parts of the globe – the ‘teleconnections’ – cause a correlated shortfall of production across multiple markets. This causes the shortages and price increases that consumers will see in their weekly shop.

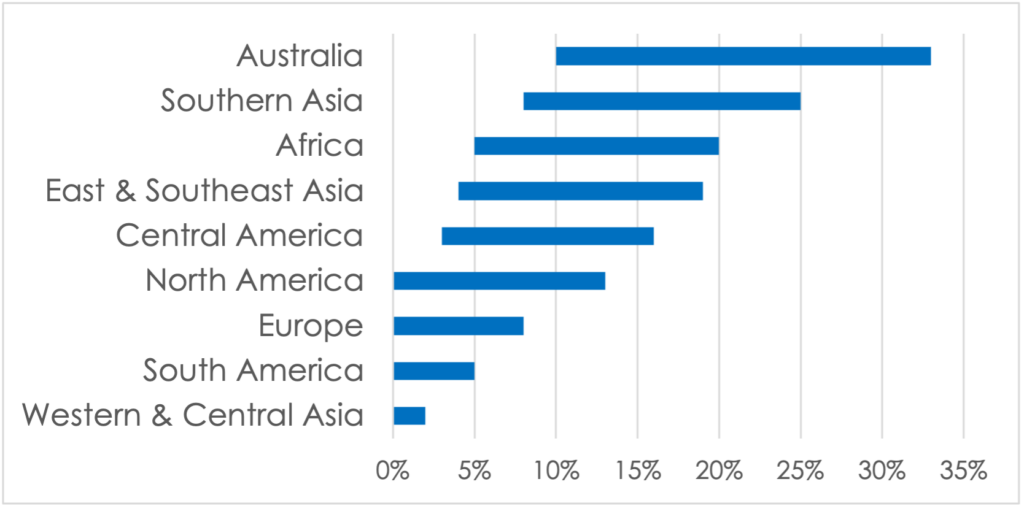

Figure 2: Agricultural Regions Most Impacted ($ Value of Key Staples Produced in Region)

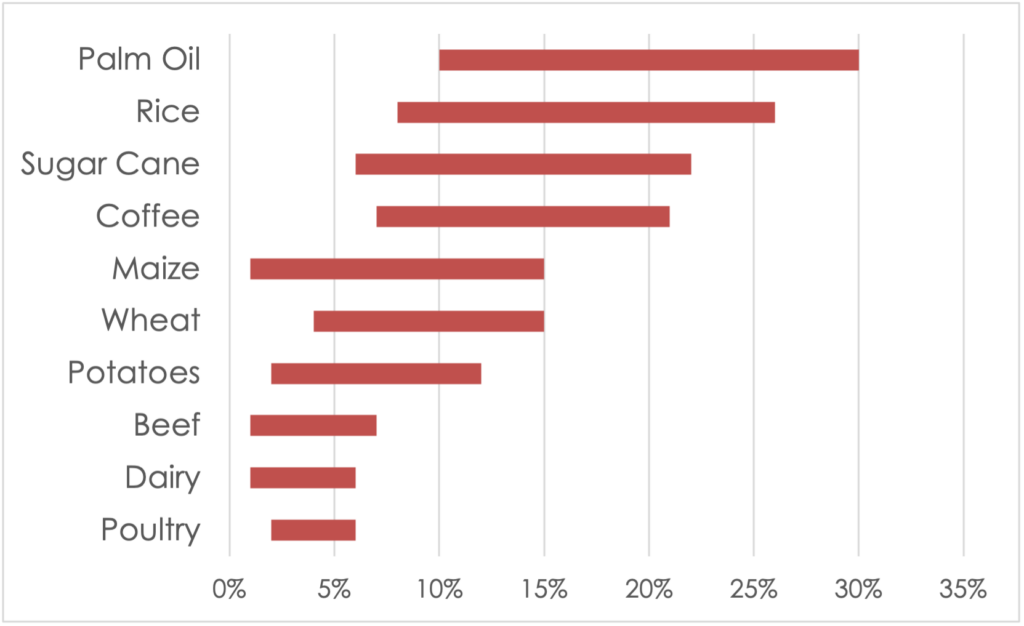

Some of the crops most at risk include rice, palm oil, sugar cane, wheat, coffee, cocoa, and potatoes. Shortfalls in crops that feed livestock, like soybeans, could cause longer-term impacts on the cost of meat and dairy.

Figure 3: Impact of el Niño Scenarios on Production (% of Global Tonnage)

A seemingly small drop in global supply can trigger disproportionately large price spikes, amplified by market panic, speculative trading, and government interventions. Some of the more severe forecasts imply levels of production shortfall that could push prices of some crops up by 50-100%. Some of the most impacted crops, such as rice, palm oil, sugar cane, and coffee could see significantly higher price surges.

The business challenge has shifted from simply enduring disruption to developing a business model prepared for permanent volatility. Forward-looking companies are developing strategies to improve the security of their agricultural supplies and minimise future cost shocks.

Building supply chain resilience involves a strategic balance between two complementary approaches: diversifying to de-risk and investing in resilient agriculture. This means reducing dependence on exposed commodities, building partnerships with growers, and investing in adaptation measures at the source.

World-leading brands are already proving the ROI of co-investing in agricultural resilience:

Where unprepared companies face catastrophic disruption, a resilient food industry has the tools to weather the storm and even strengthen its competitive position. Improving the food industry business model for reduced volatility of supply and improving the predictability of cost will require adapting current practices so that future El Niños can be managed without crisis.